In today's world, financing education through federal loans has become a common practice for many students. While it may seem appealing to borrow the maximum amount allowed, this decision can have significant long-term consequences. Understanding these repercussions is crucial for making informed choices about one’s financial future. One downside to borrowing the maximum allowed amount of federal loans is the potential for overwhelming debt that can hinder financial stability years after graduation.

When students take out the maximum federal loan amount, they often overlook the implications of such a substantial financial commitment. While it may provide immediate relief and cover tuition and living expenses, the burden of repayment can lead to stress and anxiety. Furthermore, students may not fully grasp the interest rates and repayment terms associated with these loans, which can compound the financial strain over time. This article will delve into the various dimensions of this issue, helping prospective borrowers to navigate the complex landscape of federal student loans.

In an era where education is paramount, understanding the intricacies of borrowing is essential. Students must weigh the immediate benefits of federal loans against the long-term financial obligations they incur. As we explore the downside to borrowing the maximum allowed amount of federal loans, it is important to consider not just the numbers but the overall impact on one’s life and future opportunities. With that in mind, let’s dive into the conversation surrounding federal loans and the potential pitfalls of borrowing at the maximum level.

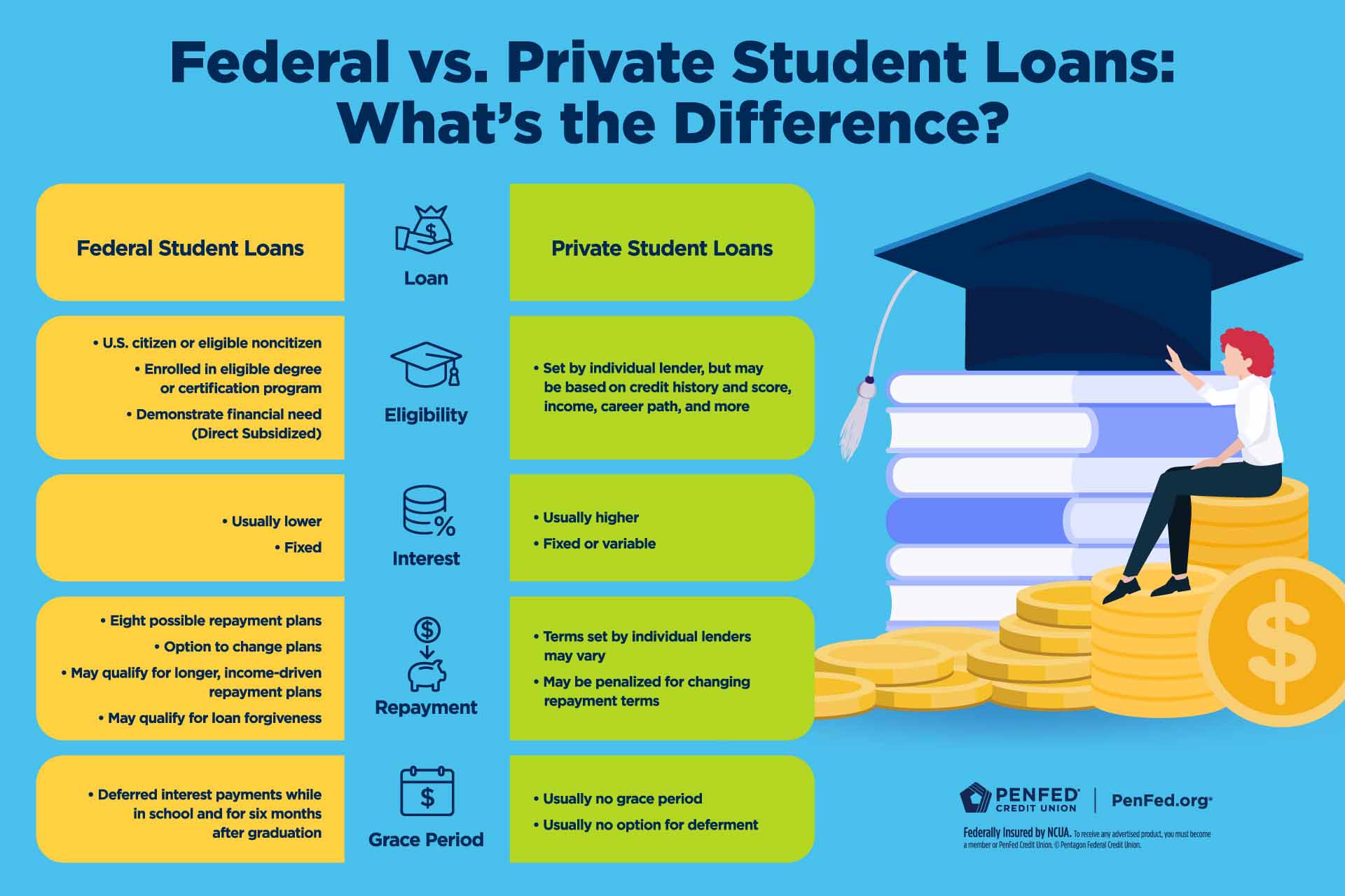

What Are Federal Loans?

Federal loans are student loans offered by the government to help students pay for their education. These loans typically have lower interest rates and more flexible repayment options compared to private loans. They come in various forms, including subsidized and unsubsidized loans, as well as PLUS loans for graduate students and parents. Understanding these loans is foundational in determining how much to borrow and how to manage the debt effectively.

Why Do Students Borrow the Maximum Allowed Amount?

Many students feel compelled to borrow the maximum allowed amount of federal loans due to several reasons:

- Covering rising tuition costs.

- Funding living expenses while studying.

- Lack of financial literacy regarding loans.

- Peer pressure to maintain a certain lifestyle.

What Is One Major Downside of Borrowing the Maximum Allowed Amount of Federal Loans?

One major downside to borrowing the maximum allowed amount of federal loans is the looming burden of debt repayment. While students may enjoy the benefits of immediate financing, they often do not realize that they are accumulating a significant financial obligation that will need to be repaid with interest. This can lead to a cycle of debt that is difficult to escape.

How Can Over-Borrowing Impact Future Financial Situations?

Over-borrowing can have a ripple effect on various aspects of a graduate's financial life:

- Difficulty in securing future loans for homes or cars.

- Increased stress and anxiety about finances.

- Limited career choices due to the need for higher-paying jobs to cover debt.

Could Over-Borrowing Affect Mental Health?

Yes, the pressure of repaying a large amount of debt can negatively impact mental health. Many students face anxiety, depression, and stress related to their financial situations, which can affect their academic performance and overall quality of life.

What Should Students Consider When Borrowing?

Students need to approach borrowing with caution. Here are some considerations:

- Assessing personal financial needs versus wants.

- Understanding loan terms and conditions.

- Exploring scholarships and grants as alternatives to loans.

- Calculating potential future earnings based on chosen career paths.

Are There Alternatives to Borrowing the Maximum Amount?

Before committing to borrowing the maximum allowed amount of federal loans, students should consider alternative funding options:

- Scholarships and grants that do not require repayment.

- Part-time work opportunities while studying.

- Income-driven repayment plans that offer more manageable terms.

How Can Students Manage Debt After Graduation?

Once graduates enter the workforce, managing their student loan debt becomes imperative. They should:

- Create a budget that prioritizes loan payments.

- Consider loan consolidation or refinancing options.

- Stay informed about loan forgiveness programs.

Conclusion: What Have We Learned About Borrowing Federal Loans?

In conclusion, while borrowing the maximum allowed amount of federal loans can offer immediate financial support, it is vital to understand the long-term consequences. The potential for overwhelming debt can create a challenging financial landscape for graduates. By weighing the benefits against the potential downsides, students can make more informed decisions about their borrowing options. Ultimately, taking a proactive approach to financial literacy and debt management can lead to a more secure financial future.